Everything You Should Know About GST – Impact of GST on Small Business

Everyone in India is talking about the upcoming GST.

Lots of our customers are from India. So, we’d thought let’s help them by explaining everything about the GST!

Today, we’re going to learn:

- What’s GST?

- GST Rates on Goods and Services

- GST Exemption List

- Impact of GST on small business

What’s GST?

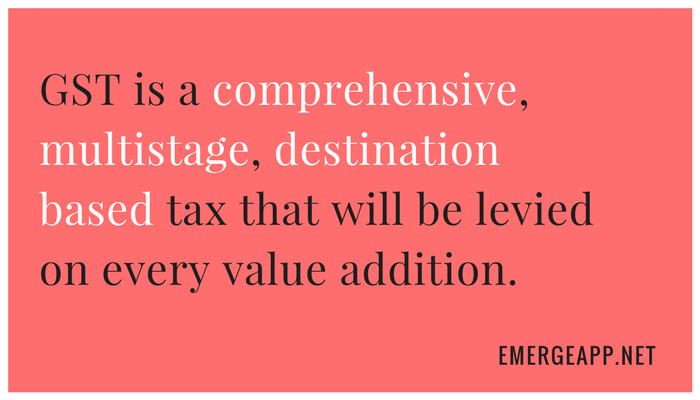

GST stands for Goods and Service Tax.

It is one indirect tax for the whole of India, which will make it one unified common market.

In essence, it is a single tax on the supply of goods and services, right from the manufacturer to the consumer. Credits of input taxes paid at each stage will be available in the subsequent stage of value addition, which makes GST essentially a tax only on value addition at each stage.

Thus, the final consumer will bear only the GST charged by the last dealer in the supply chain, with set-off benefits at all the previous stages.

In short:

Now, let’s go through what do we mean by multi-stage?

Here’s a Typical Supply Chain flow:

If you observe, this is how a product reaches the consumer. The manufacturer buys the raw materials and manufactures the product. After the product is ready, it sells the product to wholesale distributors. Wholesale distributors take their margin and sell it to the retailer. The retailer displays the product via its storefront or online to you — the end consumer.

Thus, GST will be levied on each of these stages, which makes it a multi-stage tax.

GST Rates

The Goods and Services Tax (GST) will be levied at several rates ranging from 0 to 28 percent. The GST Council has categorised it into four tiers, that is, a GST tax structure of 5 percent, 12 percent, 18 percent and 28 percent.

The lowest rates are reserved for essential items. Next, the highest for luxury and ‘demerit’ goods that will also attract an additional cess.

The service tax will range from 15 percent to 18 percent.

The lowest rate of 5 percent is for daily-use items – usual items of mass consumption.

There will be two standard rates of 12 percent and 18 percent into which the most of goods and services would fall. Most commonly used items, as well as household items, will fall under these two categories.

The highest tax slab will be applicable to ultra-luxuries, demerit and “sin” goods (like tobacco and even aerated drinks). The demerit goods will attract a cess for a period of five years on top of the 28 per cent GST.

The GST will subsume the multitude of cesses currently in place, including the Swachh Bharat Cess and Krishi Kalyan Cess and the Education Cess. Only the Clean Environment Cess is being retained.

GST Exemption List

Alcohol for human consumption will not fall under the purview of GST in India at present.

Petroleum crude, motor spirit (petrol), high-speed diesel, natural gas, and aviation turbine fuel and so on will not attract GST.

Electricity has also been exempted from GST at present.

Impact of GST on Small Business Owners

Now that you have already learned what is GST, GST slabs, and GST exemptions. Let us learn how GST is going to impact small businesses.

Small businesses will see a big transformation of the taxation system once the goods and service tax arrives.

Moreover, the new proposed system (from July 2017) will be more transparent and paperless but requires more compliance as well.

There will be an additional 36 returns per year to be filed! Thus, the small taxable person should be taken care of to avoid an unnecessary burden.

Small Business Owners Categories

- Those having turnover of up to Rs. 20 Lakh (covered under basic exemption limit)

- Those with a turnover up to Rs. 50 Lakh (exemption available in the form of composition levy)

- Those with a turnover over Rs. 50 Lakh

Small Businesses having turnover up to Rs. 20 Lakh

- The new GST law grants a basic exemption of Rs. 20 Lakh to small business owners. Suppliers shall not be liable for GST if their aggregate turnover in a financial year does not exceed Rs. 20 Lakh.

- But, if the supplier is in the following states – Arunachal Pradesh, Assam, Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh and Uttarakhand, then the exemption will be available only if the aggregate turnover in a financial year does not exceed Rs. 20 Lakh.

- Here, aggregate turnover means the aggregate value of all taxable supplies, exempt supplies, exports of goods and/or services and inter-state supplies of a person having the same permanent account number (PAN).

Small Businesses having turnover below Rs. 50 Lakh (exemption in the form of composition levy)

- Any registered taxable person can opt for the composition levy if the aggregate turnover in the previous financial year does not exceed Rs. 50 Lakh.

- It may permit the registered taxable person to pay tax under composition levy with some conditions.

- The minimum tax payable under composition levy shall be:

- 2.5% of the total revenue, in case of manufacturer; or

- 1% in any other case.

Some FAQs on the Composition Levy

Q. Who can opt for the Composition Scheme?

A. Businesses dealing only in goods can only opt for the composition scheme. Service providers have been kept outside the scope of this scheme. However, restaurant sector taxpayers may also opt for the scheme.

Q. Which returns are required to be filed by a taxable person registered under the Composite Scheme?

A. The taxable person is required to furnish only one return, i.e. GSTR-4 on a quarterly basis and an annual return in FORM GSTR-9A.

Q. What is the threshold limit to be eligible for the Composition Scheme?

A. As we already mentioned, any dealer whose aggregate turnover in a financial year does not exceed Rs. 50 Lakh can opt for the composition scheme

Conclusion

The GST is one of biggest tax reforms today in India. Small business owners should be prepared nationwide to accept this change.

I hope this article helps you out.

Good luck!

Read more: