Days Inventory Outstanding: Definition, Formula, Calculation

One of the crucial elements of running any business is how effectively one can monitor its inventory. Over the years, numerous tools and ratios have come up to assist managers to track their inventory. One such ratio is Days Inventory Outstanding (DIO).

Days inventory outstanding is a working capital management ratio used to indicate the number of days it takes for a business to turn its inventory into sales. Put simply, this ratio helps show how quickly a business is able to turn its inventory into cash.

Days Inventory Outstanding is also known as “inventory outstanding”, “inventory days of supply” or “inventory period”. While the interpretation may vary from industry to industry, a low DIO is generally an indication of optimal inventory management practice.

Calculating Days Inventory Outstanding:

The formula for calculating inventory outstanding is quite simple, contrary to what most people would be prompted to assume. Days Inventory Outstanding is calculated based on the average value of the inventory and cost of goods sold in a given reporting period.

DIO= (Average inventory/cost of sales) x Number of days in the period

-

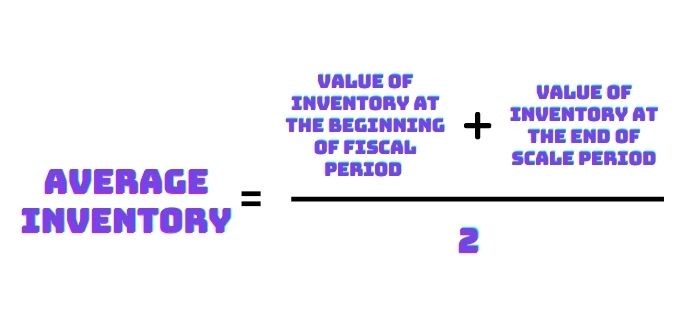

How to Calculate the Average Inventory

The average inventory is the average value of the inventory at the end of a particular reporting period and is calculated as follows:-

(Beginning Inventory + Ending Inventory)/2

An alternative formula for calculating the average inventory is:

Average inventory=Ending Inventory

This formula is however rather flawed as it does not give an accurate representation of a company’s output since most company inventories fluctuate significantly throughout the year.

For instance, most companies buy loads of goods at the beginning of the year and proceed to sell throughout the year. If we were to apply this formula, the ending inventory would therefore not mirror the actual average inventory.

Since the inventory is bound to fluctuate throughout the year, it is recommended that businesses use multiple data points in order to get a more accurate average inventory. To do this, most businesses prefer to calculate their average inventory on a monthly basis for a year plus an extra month to get 13 data points.

For example, let’s say Company A has the following:

- Beginning Inventory- $5,000,000

- Ending Inventory- $1,000,000

The average inventory for Company A shall be- $3,000,000

-

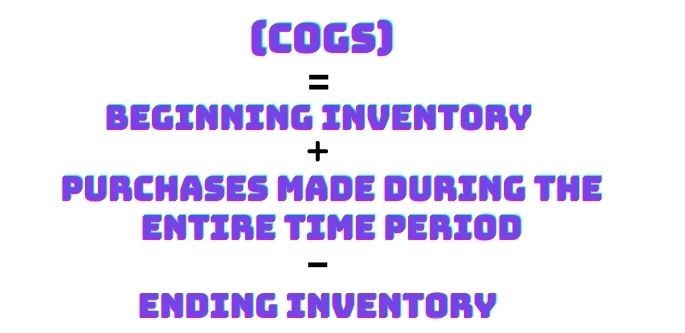

Determining the Cost of Goods Sold

The Cost of Goods Sold is defined as the cost of producing goods sold during the reporting period. This could include the cost of paying employees, buying raw materials, and payments made towards utilities such as water and electricity.

For example, let’s say Company A above has the following:

- Beginning Inventory- $5,000,000

- Purchases made during the reporting period- $ 2,000,000

- Ending Inventory- $1,000,000

The Cost of Goods Sold for Company A shall be $ 6,000,000.

It is important to note that the Cost of Goods Sold only takes into account the direct expenses of producing the goods and does not account for indirect or overhead costs such as shipping and office rent.

-

Applying the Inventory Days Formula

Using the values that we have gotten for Company A above, let’s calculate its DIO for a year:

- Average inventory- $3,000,000

- COGS- $6,000,000

- DIO- ($3,000,000/6,000,000) x 365= 182.5 days

The average inventory days for Company A are 182.5 days. Let’s find out if this is a good or bad thing for the company.

Interpreting Average Days In Inventory:

As earlier indicated, what is considered a good or bad DIO may vary from industry to industry. Regardless, a low day’s inventory outstanding is generally accepted as an indication that a company is able to quickly turn its inventory into sales.

That being said, let’s investigate the two different variations of DIO and what they indicate.

High DIO

If a company has a high DIO, the simple interpretation is that it is not churning its inventory into sales quickly, and is not managing its inventory as effectively A high DIO also indicates that the company’s cash is held up in inventory for long periods, implying it cannot be used for other purposes. Lastly, a high DIO could also be associated with overstocking, leading to a huge amount of outdated stock that may never be sold.

Low DIO

Where a company has a low DIO, it means it is converting its inventory into sales speedily. It also implies that working capital can be diverted for other pending purposes or even used to repay outstanding debt.

A company with a low DIO is also less likely to get obsolete stock that eventually has to be written off. On the downside, however, a company with low DIO may experience challenges in meeting a sudden increase in demand.

Companies Being Compared Should Exist in the Same Industry:

Why should we ensure this? Suppose Company A has a DIO of 50 days while Company B has a DIO of 250 days. Going by the rule of thumb, the automatic interpretation of this metric is that Company A is doing much better than Company B.

Realistically, this may be far from the truth. For instance, Company A could be in the business of selling furniture while Company B manufactures ships and the duration of manufacture is 180 days alone.

The point is, business operations in different industries vary, and to get a valid interpretation, you need to compare businesses in the same industry.

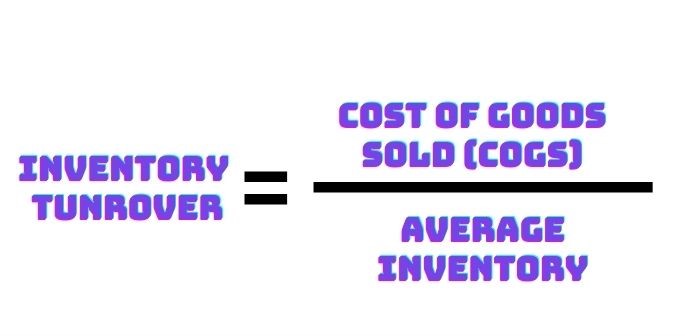

Days Inventory Outstanding v Inventory Turnover Ratio

Inventory turnover is a ratio similar to DSI and refers to the number of times a company is able to sell its inventory over a particular reporting period. Inventory turnover is calculated by dividing the cost of goods sold by the average inventory. It is also known as stock turnover, inventory turns, and stock turns.

The inventory turnover ratio helps businesses evaluate the management of inventory and how well sales are being generated. In a nutshell, this ratio helps identify how many times a company has sold and replaced inventory in a given period.

While inventory turnover helps evaluate how quickly a company can sell (turn over) its inventory, DIO helps determine the average time it takes for a company to turn its inventory into sales. Essentially, DIO is the inverse of inventory turnover in a particular period.

A low inventory turnover ratio may be considered an indication of poor sales or overstocking. It could also be an indication of an issue with the goods being sold or poor marketing.

On the other hand, a high inventory turnover ratio implies either understocking or strong sales. As with DIO, one needs to ensure that the companies being compared operate within the same industry.

Why Choose the DIO Formula?

The inventory turnover ratio is credited as being one of the best indicators of the company’s level of efficiency at turning over its inventory as well as generating sales from it. The day’s inventory is outstanding however goes the extra mile by putting that figure into a daily context and providing an accurate picture of the company’s inventory.

We can however not ignore the fact that both the DIO and inventory turnover ratio provide investors as well as management with a representation of how well a company is able to manage its inventory when compared to competitors.

For companies in the retail industry, it is considered good practice to employ both the inventory turnover ratio and inventory outstanding to effectively monitor your inventory. Both ratios offer important insights. The inventory turnover ratio helps determine how fast your business is generating the inventory while the inventory outstanding paints the same picture, only in a daily context thus creating a more holistic outlook.

Weaknesses of DIO:

Like any other ratio, the day’s inventory outstanding has imperfections such as:

- Changes in pricing– in order to clear outstanding inventory, a business may lower its prices. While this would definitely improve the inventory outstanding, it does not benefit the overall profitability of the business.

- Adjustments such as discounts/writing off stock- a company’s days inventory outstanding may be low due to inventory being written off as obsolete or being sold at large discounts.

- Changes in calculating- a company may choose to use a different method to calculate its cost of goods sold, such as by including fewer or more overhead expenses. If this change varies significantly from the method applied in the past, it may lead to an inaccurate DIO ratio.

Benefits of Using Days Inventory Outstanding:

Despite not being perfect, there are numerous benefits that a company can get from monitoring its inventory outstanding-

- Making future plans- the companies that monitor their inventory understanding are able to get a clearer picture of how their inventory fluctuates throughout the year and therefore create an accurate inventory forecast for their business.

- Helps businesses improve strategies- businesses with continuously high inventory outstanding rates are able to make informed strategic decisions such as introducing discounts or adopting new marketing styles.

- Great for businesses with perishable goods- the DIO ratio helps businesses monitor their inventory flow and therefore make informed decisions on how to stock or sell perishable goods before they go stale.

- Enhance cash flow- businesses that monitor their inventory outstanding and make effective decisions are able to free up cash that would otherwise be stuck in inventory and channel it toward other business expenses.

- Performance Indicator- the inventory outstanding ratio can be used to track the performance of management staff and to an extent even procurement staff. Investors may also use the ratio to monitor the efficacy of a business as well as its profitability compared to similar businesses in the industry.

Improving Your Days Inventory Outstanding Ratio:

As indicated earlier, the rule of thumb is that a lower DIO indicates healthy business management as compared to a higher DIO. There are several strategies that businesses can adopt to improve their day’s inventory outstanding such as:

- Employing efficient inventory management techniques such as just-in-time delivery– for companies in the production industry, just-in-time delivery frees up working capital that could otherwise have been used up buying buffer stock or raw materials.

- Disposing of outdated stock- continued monitoring of DIO helps businesses identify and dispose of slow-moving stock.

- Employ innovative marketing techniques- social media marketing has introduced new and fun ways of making clients aware of your products consequently increasing demand.

- Speeding up the sales process- the basic rule is that the faster a sale can be made, the sooner inventory is converted into cash. The sale process may be fastened for instance by introducing delivery services.

- Improving product mix- since inventory outstanding helps companies identify slow-moving goods, they can be able to capitalize on stocking more of the goods that are selling faster to maximize on profits.

- Implementing advance order books- companies can implement an advance order system to be able to effectively plan their inventory.

This being said, it is important to note that high inventory days of supply is not necessarily always problematic.

For example, a company that is anticipating a significant increase in demand may choose to maintain higher levels of inventory. The demand for some products also fluctuates seasonally and this translates into the DIO being high during the off-season periods.

Conclusion

Days inventory outstanding is a vital inventory monitoring tool and could help guide companies to make informed inventory management decisions.

Most businesses have gotten accustomed to using inventory management software, seeing as calculating inventory outstanding and turnover rates has become an essential technique of management.

It is important to note that in the current ever-changing economy, a retailer seeking growth should take advantage of technological inventory management tools such as Emerge, through which businesses are able to manage their inventory through an online inventory management solution.

This solution has been created with the understanding that most small business owners have a lot of things to juggle, and thus require all the support they can get in terms of management.

We hope that this article has provided you with a clearer understanding of days’ inventory outstanding and that you will consider employing it to monitor how fast your inventory translates into sales.